I heard a wholesaler tell someone the other day that the economy’s chugging along, all is fairly good, employment is decent, and so long as Hormuz gets opened soon, things should be back to normal in no time. I also heard him say that a Nasdaq 100 ETF that writes covered calls and generates an 11% yield is more on the conservative side. I told this person after their conversation that if he said this to 90% of Americans, he’d get punched in the nose.

Here are three charts that suggest a different story…

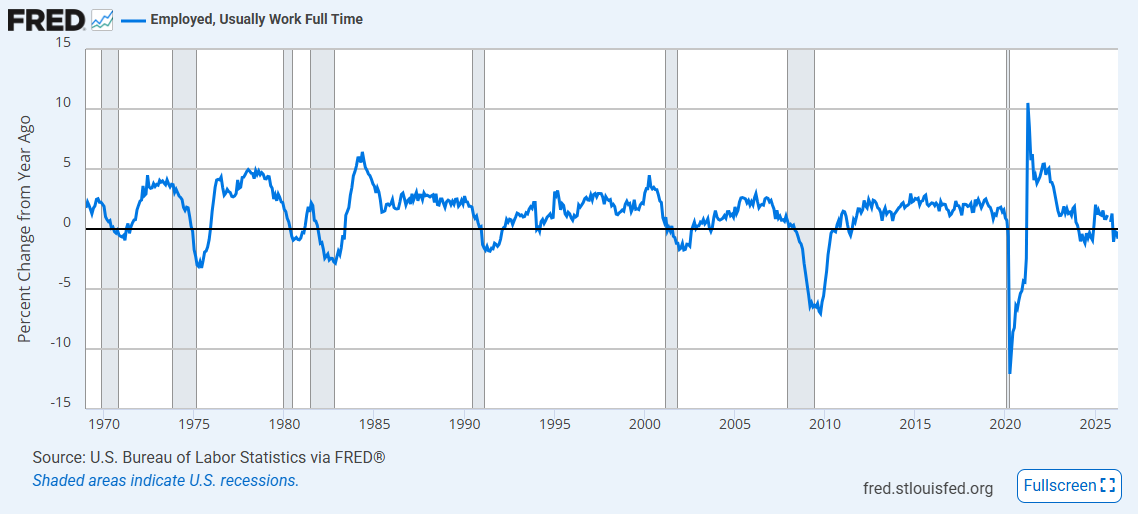

First, full-time work. Back to negative year-over-year (YOY) after the population artifact of migration worked its way out of the numbers. If you know anyone who’s recently lost a job, finding a new one isn’t easy. These numbers check out. Negative YOY growth in full-time jobs is usually reserved for recessions. Except this one, of course.

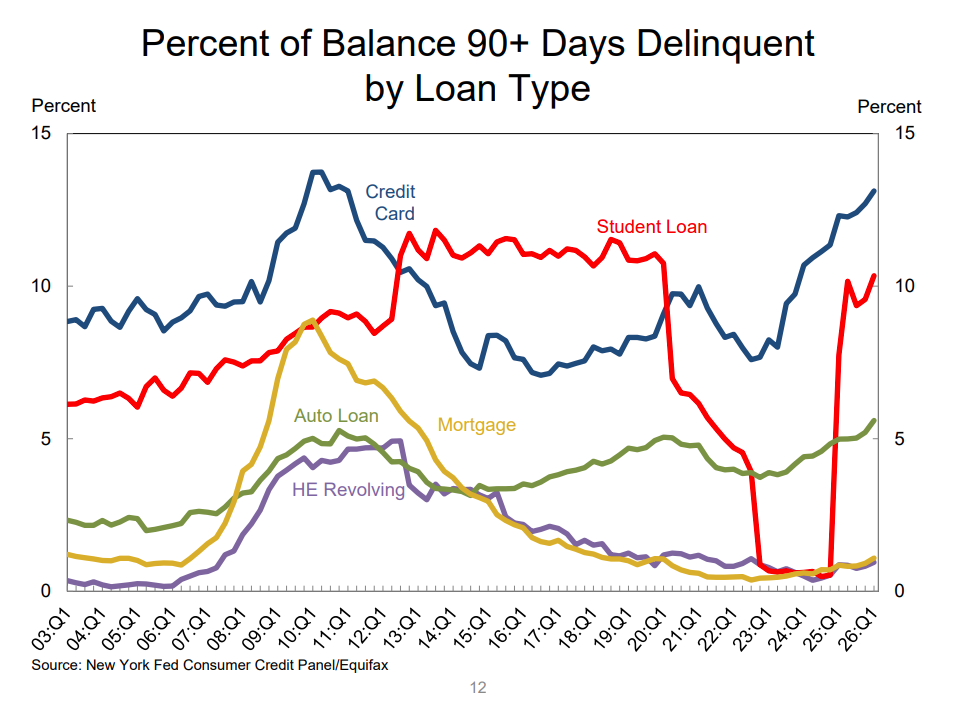

Past-due payments on various consumer loans. Not good. Student, credit card, and auto loans are higher than they were coming into the 2007—2009 recession. Mortgage and home equity are working their way up, probably still buffered by historically low interest rates from a few years ago. That is resetting every day.

Car sales. Negative YOY and declining, and with rising gas prices, folks will probably be driving even less. A decent barometer of consumer strength.

Of course, none of this means stocks can’t continue to defy gravity and logic, but it does suggest that they’re doing it on a foundation of slippery elephant dung. And, with an estimated 1.5—2 billion barrels of oil (and other important products) missing from the global economy in the months to come, “normal” probably isn’t how we’ll end up defining things.

Invest accordingly.

Important Disclosures

This blog is provided for informational purposes and is not to be considered investment advice or a solicitation to buy or sell securities. Cadence Wealth Management, LLC, a registered investment advisor, may only provide advice after entering into an advisory agreement and obtaining all relevant information from a client. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Past performance is not indicative of future results. It is not possible to invest directly in an index. Index performance does not reflect charges and expenses and is not based on actual advisory client assets. Index performance does include the reinvestment of dividends and other distributions

The views expressed in the referenced materials are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.