We’ve been hearing from multiple sources for a few years now that the United States is energy independent because we export more energy than we import. If all energy sources were interchangeable, say you could power your car with petroleum, natural gas, or coal, then maybe we’d be independent, but they’re sadly not. Likewise, even if they were interchangeable, those companies sucking petroleum and natural gas out of the ground, or gouging coal out of the earth, have the ability to sell to the highest bidders all over the world. If Australia is willing to pay $5 per gallon for gasoline, the only way that gasoline stays in the U.S. is if we are going to pay more than that; otherwise, off to Australia it goes. The fact that not all energy is the same, and even not all petroleum is the same, plus the fact that commodity markets are global, means our supposed energy independence still does not guarantee us access to inexpensive ways to power our cars and trucks, or heat our homes, which ripples through our wallets all the way to the U.S. economy itself.

Energy Sources Are Not Interchangeable

The United States has been a net total energy exporter—total energy exports have been higher than total energy imports—since 2019. Source: U.S. Energy Information Administration

That statement is technically correct, but also misleading. It aggregates crude oil, refined products, natural gas, coal, and electricity into a single heat-equivalent metric. In doing so, it collapses fundamentally different energy forms with different end uses into one number and obscures a critical reality: the United States still depends on imports of specific fuels—especially heavier crude oil—to keep its energy system running. That distinction matters because oil still dominates U.S. energy, accounting for nearly 40% of the total energy consumed.

Oil is not just another fuel; in some senses it IS the economy. It powers transport, agriculture, mining, and construction, and it underpins global trade. Most goods either contain oil, or depend on it somewhere in their supply chain, or both. When oil flows smoothly, the economy functions. When it doesn’t, everything slows, breaks, or gets more expensive – as we are seeing today at the gas pumps and in other places. We may already be seeing price increases in products that need to be transported around, but what we probably have not

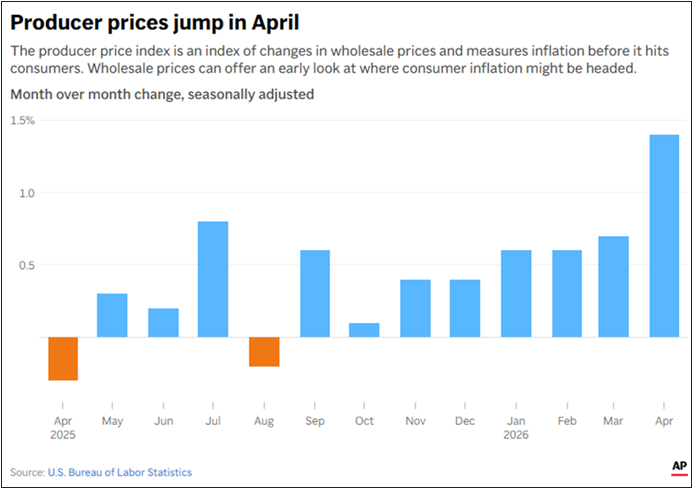

seen much of yet are price increases caused by the rising costs of making products, which is measured by the “producer price index”. It takes time to manufacture something. As a result, it also takes time for the increased cost to manufacture that something to be passed on to consumers, depending on what that something is.

The chart below shows that producer prices were already elevated the first few months of this year, followed by a meaningful jump in April.

If the manufacturers don’t absorb all these elevated costs and instead pass them along to consumers, that process takes a few months before those production costs ripple out into prices at the stores. Because energy sources are not interchangeable, the supposed energy surplus the U.S. runs still does not prevent price spikes in certain energy sources, such as crude oil, from acting as a drag on household finances, and therefore the broader U.S. economy.

With All Our Oil Production, Why Do We Still Import Oil?

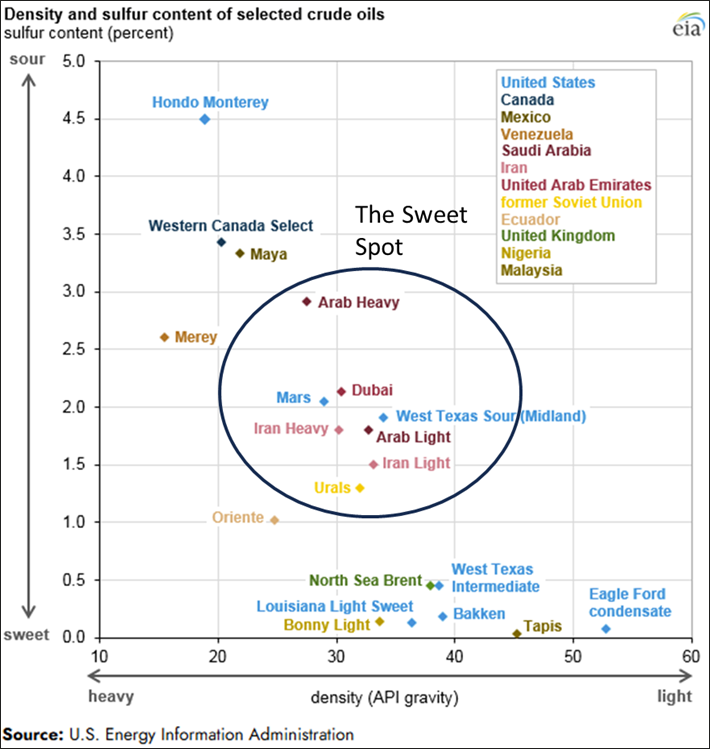

Despite our net energy exporter status, the United States still remains a substantial net importer of crude oil. Imports averaged about 6.3 million barrels per day in 2024 and 2025, while exports were only about 4.0 million barrels per day. Why does the U.S. both import and export large volumes of crude oil? Because not all oil is the same. Most U.S. oil production is categorized as light and sweet crude. Many U.S. refineries, however, were built to meet strong demand for diesel and jet fuel, which require heavier, sour crude in the mix. The refineries were designed to run that heavier oil alongside lighter barrels. The U.S. shale boom flooded the system with light, sweet crude that refineries weren’t configured to fully absorb, creating a persistent surplus in some oil, and a persistent shortage in other oil.

Middle Eastern oils sit near the global “sweet spot”—balanced in a way that allows refineries to produce gasoline, diesel, and jet fuel efficiently with minimal adjustment. This is one reason why even though only 20% of the world’s crude flows out of the Middle East, it is having such a massive effect on global gasoline prices. A shortage of the very best oil is not easily balanced by making up that difference by combining the lower quality oils. Many global refineries use some light oil like U.S. shale and some heavy oil like Canadian or Venezuelan crude, but the backbone of the system is medium-grade oil from the Middle East.

The U.S. uses as much of its own light oil as it can, exports the surplus, and imports heavier crude—mainly from Canada—to complete that blend. Even as the world’s largest producer, the U.S. still depends on imports. As long as the U.S. requires foreign crude to produce usable gasoline, it’s not energy independent—no matter what anyone says, and no matter how much total energy we create above the total we consume. Even if we did produce the perfect mix of light and heavy crude, we probably still wouldn’t be energy independent because the rest of the world would be incentivizing our producers to send the oil their way by bidding up the price. We are more interdependent than independent when it comes to the price we pay for a gallon of gas, and that interdependence is leading to elevated prices despite our net energy exporter status.

The Difference Between Energy Independence and Energy Security

It sounds straightforward in its wording, but energy independence has always been an ill-defined, unachievable goal. Depending on whom you ask, it means reaching self-sufficiency in energy production or immunity from foreign turmoil. But even if the U.S. sourced every drop of oil we use from within our own borders, we would still be vulnerable to international price shocks because oil is a globally traded commodity. Its price is not set by how much the U.S. extracts at home, but by the laws of international supply and demand. A disruption in the flow of oil anywhere affects prices everywhere.

It may not sound as good, but a better goalpost than “energy independence” is “energy security,” meaning an uninterrupted flow of hydrocarbons and electrons at an affordable price. That requires both strong domestic production and secure sources from abroad. For the most part, that is what we have enjoyed for the past 35 years, with the average price per gallon of gasoline in the country at $3.00 or less over 70% of the time since 1990, per the U.S. Energy Information Administration.

To really maximize energy security, the U.S. would need to minimize the way energy price volatility can affect our economy, and we are years and years away from that, if we are even trying to achieve it at all. Even were the U.S. to create policies saying all oil produced in the U.S. has to stay in the U.S., the fact that we don’t produce enough heavy crude means that policy wouldn’t help much – we would still need to import the type of oil we cannot produce enough of ourselves. There are a lot of opinions on how the U.S. could increase its energy security, with many of them contradicting the others. Suffice to say that without true energy security, our economy and our wallets will continue to feel pain any time the supply of energy gets reduced, as the flow of crude oil out of the Middle East has been the past few months. Until then, it is up to all of us individually to shield ourselves from the effects of higher energy prices.

We frequently talk about times like these when we are planning, these theoretical times where we may need to tighten our belts one or two notches. We probably have not yet seen how expensive many of our necessities are going to get. Even though almost all Cadence portfolios have some investments benefitting from higher energy prices, now is still a time to consider keeping a closer eye on spending. We do not know how high oil prices may rise, nor when the flow of the crude that U.S. oil companies cannot produce enough of will increase again, but we do know we have the ability to adjust your financial plan to match this scenario. We cannot change what the world’s energy prices throw at us, but we can plan for it.

Editor’s Note: This article was originally published in the June 2026 edition of our Cadence Clips newsletter.

Important Disclosures

This blog is provided for informational purposes and is not to be considered investment advice or a solicitation to buy or sell securities. Cadence Wealth Management, LLC, a registered investment advisor, may only provide advice after entering into an advisory agreement and obtaining all relevant information from a client. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Past performance is not indicative of future results. It is not possible to invest directly in an index. Index performance does not reflect charges and expenses and is not based on actual advisory client assets. Index performance does include the reinvestment of dividends and other distributions

The views expressed in the referenced materials are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.