One of the most dangerous delusions being pumped and disseminated by Wall Street today is that the economy and stock market can and should continue to thrive indefinitely without interruption. Wall Street is notoriously perma-bullish based on its business model being dependent on steady investment inflows, so for those paying attention, it’s no surprise why its foot soldiers don’t express opinions through the financial media or otherwise that are counter to this perpetually rosy view. More recently, and it’s been increasing in intensity over the last couple decades at least, the Federal Reserve has taken it upon themselves to attempt to eliminate the downward part of the business cycle. In his latest Jackson Hole speech, Fed Chairman Jerome Powell pledged to “act as appropriate to sustain the expansion”. This while we sit atop one of the longest economic expansions and the most expensive stock and bond markets in all recorded history.

While Wall Street’s interest in delaying the downward part of the cycle is profits, the Federal Reserve’s must be something else, right? Why would the institution that was established more than 100 years ago stray so far from its initial charge as lender of last resort in the event of financial crisis? We’ve drifted from the Fed serving as disaster insurance to it being the arbiter of more growth at all costs. In an attempt to deliver on this “new” objective, the Fed and other central banks have created an Alice in Wonderland-type world where the reality around us just boggles the mind.

- We have a debt problem and because people (including corporations and governments) are paying too much toward the interest on that debt, they aren’t buying as much stuff anymore. Hmmm, how do we solve this? Let’s get them buying again by lowering interest rates and encouraging more debt. Right, that’s a brilliant long-term solution to the problem, which of course is not enough buying rather than too much debt.

- To encourage this buying, we need to make sure that we create inflation of let’s say, hmmm, 2%. That should get people buying things if they think it’ll cost them more in the future. This also must be a good solution to the problem, which of course is not enough people buying stuff rather than the cost of living being too high for the average American to begin with.

- Let’s consider lowering interest rates to 0% to really encourage these two things to happen quickly before we see the cost of goods go down (deflation). Of course, every American knows that the cost of things they need to buy going down is a horrible specter that should be avoided at all costs. Before this doomsday scenario plays out, we need to cut rates to 0% in order to generate new debt-fueled consumption and inflation. Right. That’s obviously a brilliant long-term solution to the problem, which of course is the threat of a lower cost of living for the majority of Americans rather than retirees not being able to earn any interest on their bank deposits. We clearly have our priorities straight and are unquestionably looking out for the average American with this one.

- And if that doesn’t work, we’ll consider negative interest rates, where you actually pay the government to lend them money. Michael Lebowitz of 720 Global had a great quote regarding this concept. He raised the question “If you borrow money from a loan shark at a negative rate, do you break his kneecaps if you don’t repay?” Fair question that deserves a fair response from the Fed.

The intentions of those pulling the levers are either misguided, naïve or just morally impure. We won’t opine as to what the true motives are for the Federal Reserve’s actions, but what we will say, in addition to Jerome Powell having lots of assets that he’d rather not lose in a cyclical downturn (over $100 million worth), is that motives ultimately won’t matter because nobody can eliminate the rather scientific and mathematical concept of the cycle.

We’ve written about this concept fairly regularly. The cycle can get extended, muted, stretched-out, but it ultimately cannot be eliminated. We may in fact be at that point now where the weight of all the misallocation of resources, excessive speculation, and debt is beginning to exert its downward force on the economy and markets despite the Fed’s best efforts. At some point, doing more of the same stupid stuff that got you in trouble in the first place just plain stops working. It’s somewhat akin to piling lie on top of lie to keep from facing the music. Eventually, it’s not the first thing you did that’s the problem anymore. It’s all the subsequent confections that created the real monster. The additional debt accumulated and lack of deposit growth for savers and retirees after years at too-low interest rates has actually had the opposite effect of that intended. The same levers that once stimulated a quick economic response are much less effective now. The monster is choking on its last meal. No more. This phenomenon is often referred to as “pushing on a string”, which we think is an apt metaphor, and it certainly seems that this is exactly what central banks around the world are currently doing.

The global economy and markets are facing difficulty at the moment. Despite the best efforts of some to declare otherwise, we’ve been facing a cyclical deceleration in growth for months now and it has central bankers in a bit of a panic. They know the consequences if they lose the handle. They know that given the new world they’ve created, they can’t afford to wait until we actually experience a crisis before acting, they need to be quick to prevent that first domino from falling. This helps to explain the mind-bending policies and actions that have been taken lately. The system has been turned inside-out to prevent it from naturally re-balancing itself. Importantly, despite this, we’re still seeing a strong gravitational pull on the economic, credit, and market cycles.

Here’s what we’re observing:

- Global stock markets peaked in January 2018 and are -15% lower since

- U.S. stocks per the S&P 500 are flat since their first peak on January 26, 2018, 19 months later

- Over half of global manufacturing indexes (Global PMI’s) are in contraction (below 50)

- A host of U.S. leading economic indicators peaked in the third quarter of 2018 and are currently in decline toward contraction.

- Credit spreads between junk-rated debt and investment-grade debt are rising, indicating a shift from risk-seeking toward risk-avoidance

- Against the backdrop of these aforementioned factors, defensive asset classes such as precious metals and U.S. government bonds have begun trending higher

Investment Implications

The question investors should be asking is, when the cycle turns, what will it do to the forward returns of various asset classes? Last year, we wrote a couple letters discussing not just the danger in being too exposed to stocks, but the opportunity in precious metals and government bonds when that turn in the cycle ultimately arrives.

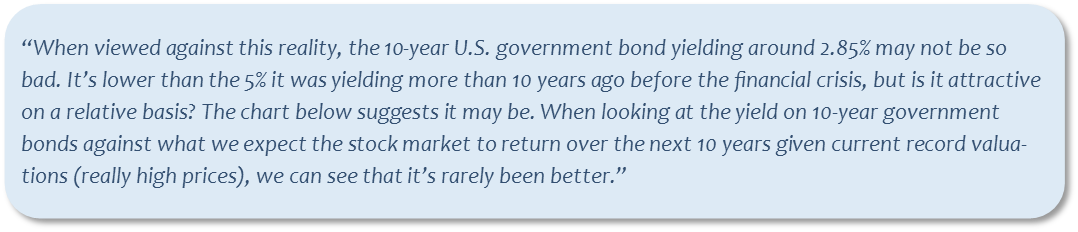

In June of last year, we shared these thoughts on U.S. government bonds…

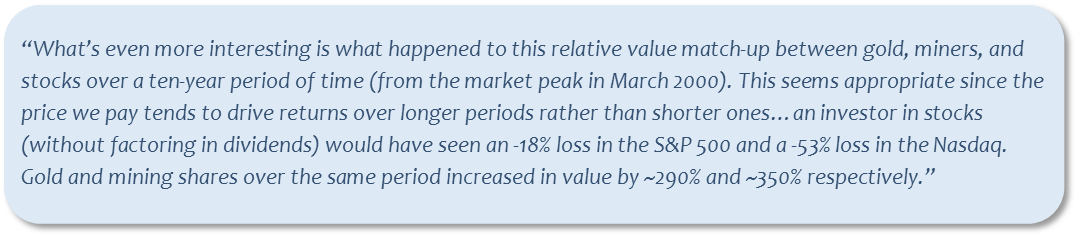

In the same June letter, we discussed these aspects of precious metals…

Our rationale for these comments was simply price and value. The trends that provided yesterday’s returns will at some point reverse and detract from those returns. At the same time, the trends that delivered yesterday’s losses will at some point abate and leave certain asset classes attractively priced. When talking about broad, longer-term cycles, it really is as simple as this. Timing is nearly impossible to pinpoint, but cycles always both giveth and taketh away. Add to this the magnitude of the central bank policy actions today and we have a much stronger potential tailwind behind these defensive, safe-haven categories if risks materialize suddenly and dramatically.

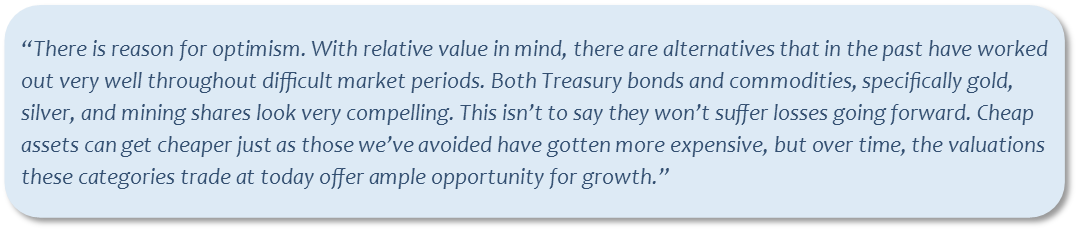

Since our June 2018 letter, here is a look at how gold, silver, gold miners shares, and U.S. government bonds have performed relative to U.S. stocks:

To sum up the chart above, here’s a breakdown of performance since then:

- Gold miners (GDX) – Up 36%

- U.S. Government Bonds (TLT) – Up 23%

- Gold (GLD) – Up 21%

- Silver (SLV) – Up 13%

- U.S. Stocks (S&P 500) – Up 8%

- Global Stocks ex-U.S. (MSWorld) – Down 7%

Even more importantly, since the global stock market peak in late January 2018, here are the performances of these same holdings (as shown in the chart below):

- Gold miners (GDX) – Up 32%

- U.S. Government Bonds (TLT) – Up 24%

- Gold (GLD) – Up 16%

- Silver (SLV) – Up 10%

- Stocks (S&P 500) – Up 7%

- Global Stocks ex-U.S. (MSWorld) – Down 15%

These categories that had been underperforming stocks for quite some time have finally started to outperform and given what we’ve observed about the broader economic and market cycles globally, this is significant. It could very well indicate a wholesale shift in investor preference away from those assets that are historically overpriced into those that offer more long-term value. These shifts tend to be subtle at first, then more dramatic and pronounced as others start to pick up on what’s happening, which helps to explain the rapid price increases of these categories over the last three months. What we’ve noticed in prices as well as the media’s increased attention to the matter over the last few weeks suggests that this shift may be just starting to pick up steam.

This isn’t to say there won’t be volatility from day to day, but it’s important for long-term investors to keep in mind that the potential for future gain is based on the attractiveness of an asset class’s price today. In this respect, the oncoming change in the cycle should play out over months and years rather than days and weeks. Of course, we’ll continue to monitor the bigger picture to see whether the Federal Reserve and global central banks can further delay the arrival of the cyclical downturn, but regardless, the risk/reward dynamic of these safe-haven categories continues to look very compelling.

There are reasons why central banks haven’t returned to “normal” interest rates – rates that conservative investors need to safely outpace inflation. They simply can’t. Returning to a 5% CD world is the enemy of a financial system that’s grown accustomed to borrowing at 2%. This reality should be a wakeup call to investors everywhere that central banks have created a world from which there is no easy exit. Pensioners should think about how their monthly benefits might be affected if the portfolios backing them can no longer achieve their 7% long term growth objectives. We should all think about the ramifications of attempting to solve the problem of too much debt by encouraging more debt. Common sense tells us this is not an intelligent solution and it cannot end well. Beyond this, we actually have empirical evidence from Japan and Europe, and more recently here at home, that this solution simply has not worked with respect to increasing economic output and long-term prosperity for the masses – unless of course we define economic prosperity as temporary stock market gains here in the U.S. (Japan’s stock market has grown by ~1% per year since 2007 while Europe’s has lost value since then, so there’s good reason to believe that the success the Fed has had in driving markets higher will in fact prove to be a flash in the pan). It’s when we think these things through to their logical ends that we realize central banks will not save us from deep stock market losses. If anything, they will only succeed in making them worse. The fact that so many investors believe that central banks are infallible and possess the solutions to all the world’s problems has only provided more fuel for the fire that has the potential to intensify the next cyclical downturn – the very one we may be in the process of observing right now.

Despite all the monetary chicanery taking place today by the Fed and its global counterparts, cycles will play out. Investors need to stay focused on the end game. Over time, prioritizing price and risk-management will no doubt help to keep investors safer and reward them with a superior end result rather than a shiny ephemeral one. The good news is that investors who’ve been preparing for the inevitable change of seasons are currently being rewarded for their patience – handsomely.

Editors Note: This article was originally published in the September 2019 edition of our “Cadence Clips” newsletter.