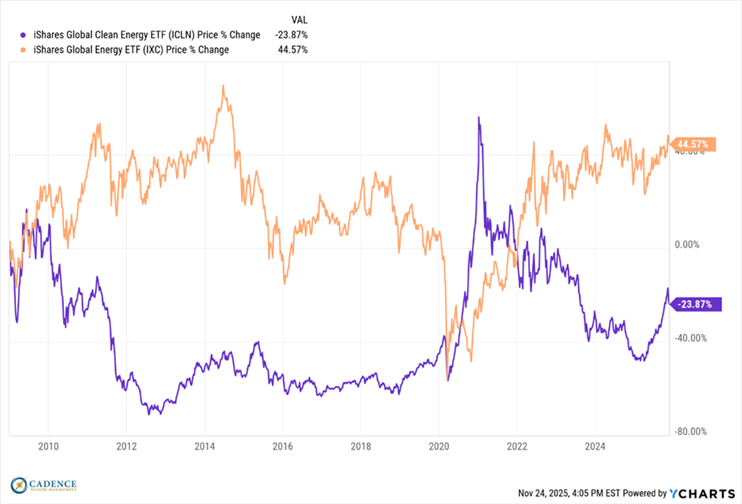

There aren’t many people out there that don’t care about the environment. There also aren’t many people out there who would willingly pay more for an energy source that didn’t offer clear advantages over less expensive ones, but a narrative can go a long way toward shaping perception and behavior despite the facts underlying it. Take the “clean energy” movement that created almost as much hype among investors as it did profit for Wall Street. The gist, as we’re all very familiar with given its proximity to the Climate Change narrative, is that traditional oil and gas energy is dirty, full of CO2, and therefore wrecking the planet, while wind, solar, geothermal, biomass, and others are clean, sustainable, and virtuous. This sounds really nice on its face, except for the fact that most of it isn’t nearly as true as the narrative would have investors believe. We won’t get into the details since most have been conditioned to view issues like these politically (by design), but suffice it to say that the clean energy movement hasn’t delivered on the key aspects of its promise. Benefits have fallen well short in that the intermittency of wind and solar have limited its usefulness in large scale applications. The risks have been much greater than were initially discussed in that the cost of electricity in areas that have integrated large scale wind and solar are higher than in areas that haven’t. And the focus on it being clean, which is supposed to get you thinking about CO2 only at the time of use and not production, completely ignores other environmental impacts at every step in the lifecycle of wind, solar and other “clean” energy solutions. The final litmus test, however, is how companies that deal in these technologies have performed over time. As we can see below, from 2009 to present, a portfolio of clean energy companies has fairly dramatically underperformed a portfolio of traditional energy companies. The ETFs being compared are both iShares and both global. A good, sustainable technology that makes sense to the average consumer should be able to stand on its own and deliver a profit to the company delivering it, without pressure, and free of subsidy. If it can’t, this is a tell that we should all be asking more questions. Even more so if the risk/benefit calculation doesn’t balance.

What’s important to note is that this narrative, although deflating in real time, isn’t finished just yet. The clean energy ETF (ICLN) shown in the chart to the left, still has a price to sales ratio of 5.7 and a price to book ratio of 6.2 compared to those of the traditional energy ETF (IXC) at 2 and 2.2 respectively. Put simply, the clean energy investment portfolio is still priced almost 3 times more expensively than a traditional energy fund, in large part due to the lingering narrative around clean energy playing a much bigger role in the future than it does now. It’s worth noting that in addition to price performance being better over the last 16 years for traditional energy stocks (IXC), they also continue to pay a dividend that’s more than 2x that of the clean energy ETF (ICLN), at 3.6% versus 1.6%.

If the clean-energy promise were truly realistic, the current landscape would look very different. Valuations would be more reasonable and stable, dividends likely higher, and share-price behavior healthier and trending upward. The reality—if we’re being candid—is that the bulk of the money being made from the clean-energy narrative is flowing to those promoting the “clean and green” story, not to the investors buying into it through public markets. As with many ideas that appear obvious and virtuous, there is often more to the story—and the lion’s share of the benefits typically flows to the storytellers.

Editor’s Note: This article was originally published in the December 2025 edition of our Cadence Clips newsletter.

Important Disclosures

This blog is provided for informational purposes and is not to be considered investment advice or a solicitation to buy or sell securities. Cadence Wealth Management, LLC, a registered investment advisor, may only provide advice after entering into an advisory agreement and obtaining all relevant information from a client. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Past performance is not indicative of future results. It is not possible to invest directly in an index. Index performance does not reflect charges and expenses and is not based on actual advisory client assets. Index performance does include the reinvestment of dividends and other distributions

The views expressed in the referenced materials are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.